Kentucky Rural Housing USDA loans require One of the biggest eligibility requirements is that the property be located in a designated rural area of Kentucky.

You can use this map for Kentucky USDA Rural Housing Eligible Areas below to determine if the property you have your eye on is eligible for a Kentucky USDA home loan.

There are some smaller towns like Frankfort, Richmond, Winchester, Bowling Green, Paducah, Owensboro, Henderson and Radcliff that are not eligible for the USDA loan program--(see brown shaded areas on map link)

The second crucial element for qualifying or a USDA in Kentucky is the income limits. USDA income limits can’t make more than 115% of the median family household income for the area in which you wish you purchase the home.

With regard to income, the max DTI ratio is 29/41, meaning the housing payment can’t exceed 29% of gross monthly income and total liabilities can’t exceed 41% of income. You can go higher with an automated GUS approval.

You must also occupy the property you’re buying – no second homes or investment properties are permitted. But manufactured homes are USDA eligible. And there area loan limits just like there are on conventional mortgages and FHA loans..

The Kentucky USDA home loan program is not limited to just first-time home buyers. Repeat buyers are also eligible!

Types of Kentucky USDA Home Loans

The USDA home loan only comes in one flavor; a 30-year fixed-rate mortgage. Nothing fancy or exotic here to ensure borrowers don’t get into any trouble with an ARM.

The 15-year fixed also isn’t an option because such a loan would imply that the borrower could afford a conventional loan and not need to rely on the USDA and its zero down financing program.

However, you can use a USDA home loan to both purchase a new property or refinance your current mortgage under certain circumstances. But no cash out is permitted if you perform the latter.

There is a sister program known as the Section 502 Direct Loan Program that assists low- and very-low income borrowers by providing subsidies that lower monthly mortgage payments for a select period of time.

The income limits for this program are significantly lower than those for the main USDA loan program, but the benefits are pretty amazing. For example, you can obtain an interest rate as low as 1% and get a 38-year loan term.

Minimum Credit Scores for a Kentucky USDA Home Loan Approval

Technically, there is no minimum credit score required to obtain a USDA home loan. However, lenders often impose overlays over USDA guidelines to ensure the borrowers are creditworthy.

Generally, you’ll need a credit score of 640 or higher to get approved for a USDA loan, though it’s possible to go lower with an exception or a manual underwrite.

When doing a manual underwrite, you should have compensating factors (such as long-term employment, assets, decent income, positive rental history etc.) to allow for the lower credit score. Your mortgage rate will also be higher to account for increased risk.

Also note that a higher credit score may be required if your DTI exceeds the allowable ratios.

In any case, you should really try to attain much higher credit scores if you want to get any type of mortgage, and favorable terms on said loan.

As with any other mortgage, it’s advisable to check your credit several months in advance to ensure your credit is on good shape, and if not, take steps to improve it before applying.

Credit score over 680:

Perform a basic level of underwriting to confirm the

applicant has an acceptable credit reputation. Perform additional analysis if the

applicant’s credit history has indicators of unacceptable credit as noted in Paragraph 10.7

of this Chapter.

Credit score 679 to 640:

Perform a comprehensive level of underwriting.

Underwrite all aspects of the applicant’s credit history to establish the applicant has an

acceptable credit reputation. Credit scores in this range indicate the applicant’s

reputation is uncertain and will require a thorough analysis by the underwriter of the

credit to draw a logical conclusion about the applicant’s commitment to making

payments on the new mortgage obligation. The applicant’s credit history should

demonstrate his or her past willingness and ability to meet credit obligations.

Credit score less than 640:

Perform a cautious level of underwriting. Perform a

detailed review of all aspects of the applicant’s credit history to establish the applicant’s

willingness to repay and ability to manage obligations as agreed. Unless there are

extenuating circumstances documented in accordance with this Chapter, a credit score in

this range is generally viewed as a strong indication that the applicant does not have an

acceptable credit reputation.

Little or no credit history: The lack of credit history on the credit report may be

mitigated if the applicant can document a willingness to pay recurring debts through

other acceptable means such as third party verification or cancelled checks. Due to

impartiality issues, third party verification from relatives of household members are not

permissible. Lenders can develop a Non-Traditional Credit Report for applicants who

do not have a credit score in accordance with Paragraph 10.6 of this Chapter.

An applicant with an outstanding judgment obtained by the United States in a

Federal court, other than the United States Tax Court, is not eligible for a guarantee

unless otherwise stated in this Chapter.

Validating the Credit Score.

Two or more eligible trade lines are necessary to validate

an applicant’s credit report score. Eligible trade lines consist of credit accounts

(revolving, installment etc.) with at least 12 months of repayment history reported on the

credit report. At least one applicant whose income or assets are used for qualification

must have a valid credit report score.

Confirm the applicant has at least two eligible tradelines reported to the credit bureau.

The tradeline may be open, closed and/or paid in full by the applicant. Eligible tradelines

include:

Loan (secured or unsecured);

Revolving (generally a credit which is not repaid by a certain number of

installments);

Installment credit (generally repaid through a specified number of

installments such as automobile, recreational vehicle, or student loans);

Credit card (offered by banking institutions, commercial enterprises and

individual retail stores. Consumers make purchases on credit and if payment

is made within a stipulated period of time, no interest is charged);

Collection (an account whereby an original creditor transfers an unpaid,

delinquent balance to a collection agency to retrieve any monies owed);

Charge-off (is the declaration by a creditor that an amount of debt is unlikely

to be collected)

Authorized user accounts may not be considered in the credit score and credit

reputation analysis unless the applicant provides documentation that they have

made payments on the account for the previous 12 months prior to

application.

Indicators of unacceptable credit.

Foreclosure within 3 years:

Including pre-foreclosure activity, such as a pre-foreclosure sale or short sale

in the previous 3 years\

Bankruptcy within 3 years:

Chapter 7 bankruptcy discharged in the previous 3 years;

An elapsed period of less than 3 years, but not less than 12 months, may

be acceptable if the applicant meets the criteria of Section 10.8 of this

Chapter.

Chapter 13 bankruptcy that has yet to complete repayment (repayment plan in

progress) or has completed payment in the most recent 12 months.

Plans that are completed for 12 months or greater do not require a credit

exception in accordance with Section 10.8;

\

Kentucky USDA Home Loan Mortgage Insurance Costs

One of the upside of the USDA home loan is the fact that there’s an upfront guarantee fee that the borrower must pay. It is currently set at 1.0% of the loan amount, and .35% monthly mi premium called the annual fee, which is much cheaper than FHA and Conventional loans on lower credit scores.

This can be financed into the loan amount so it’s paid off over time, as opposed to upfront out-of-pocket at closing. And if the USDA guarantee fee is financed the LTV can exceed 100%.

Refinancing a Kentucky USDA Home Loan

It’s also possible to refinance an existing USDA home loan into another USDA loan, and actually quite easy thanks to a streamlined program that doesn’t require an appraisal, credit report, or a debt-to-income calculation.

The only requirement is that you must have been current on your mortgage for the past 12 months, and it must lower your interest rate by at least 1%.

There is also a non-streamlined USDA refinance option that requires an appraisal to gain approval, but allows you to roll closing costs into the new loan.

Kentucky Rural Housing USDA Home Loan Frequently Asked Questions

Do I need to make a down payment on a USDA home loan?

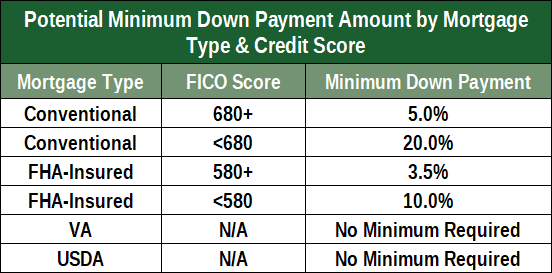

No, you can obtain 100% financing with a USDA loan, which is the main draw of the program. The only other government housing loans that provide zero down financing are VA mortgages.

What credit score do I need to get a USDA loan?

You need a 640 credit score to get an automated approval for a USDA loan, but some lenders will go to 581 with expensive pricing adjustments. If you have bad credit, you may want to take a hard look at your credit history and clean it up as much as possible before applying.

Do I need two years of job history to get approved for a USDA loan?

Not necessarily. If you’re new to the workforce or returning after a reasonable and explainable absence and likely to continue working it may be permitted.

Can I get a USDA loan if I’m self-employed?

Yes, but you’ll need to provide two years of tax returns to ensure it is stable and in the same line of work.

Are USDA mortgage rates high or low?

They’re generally pretty low relative to conventional mortgage rates (Fannie and Freddie) and pretty close to FHA mortgage rates. If an FHA 30-year fixed is 4.5%, the USDA 30-year fixed rate might be 4.5%. In other words, they’re low and competitive.

But you have to factor in the upfront and monthly mortgage insurance premiums as well.

Additionally, USDA loan rates can’t be more than 1% above the current Fannie Mae yield for 90-day delivery for 30-year fixed rate conventional loans. This regulates how high the rate can be based on the market average.

What loan types are available via the USDA loan program?

Just the 30-year fixed. No adjustable-rate mortgages and no other fixed products are available. Additionally, balloon mortgages and interest-only mortgages aren’t permitted, nor are prepayment penalties.

Can you buy a condo with a USDA home loan?

Yes, but it must be on the approved list from Fannie/Freddie, the FHA, or VA, and it must be located in a rural area.

Can I get a USDA loan on a second home or investment property?

No, USDA loans are only available on owner-occupied primary residences.

Can I get cash out via a USDA loan?

No, only rate and term refinances are available, along with purchase financing.

Can I roll closing costs into a USDA loan?

Yes, as long as the property appraises for more than the purchase price and the DTI isn’t exceeded as a result. You can also use seller concessions or a lender credit to cover closing costs.

Is there mortgage insurance on a USDA loan?

It’s technically called a guarantee fee, and includes both an upfront fee at closing (that can be financed) and a monthly fee that is ongoing.

!

How long does it take to get a USDA loan in Kentucky?

Like all other mortgages, it depends on your specific scenario, but the USDA loan approval process does require an extra step in sending the loan to the USDA for final approval. They basically check the lender’s work before they allow them to fund the loan. This step can add an extra few days to few weeks (or more) onto your closing date, so beware!

Kentucky USDA Rural Housing Map Below:👇 Click on link below to see if the home is located in a Rural Housing Area.